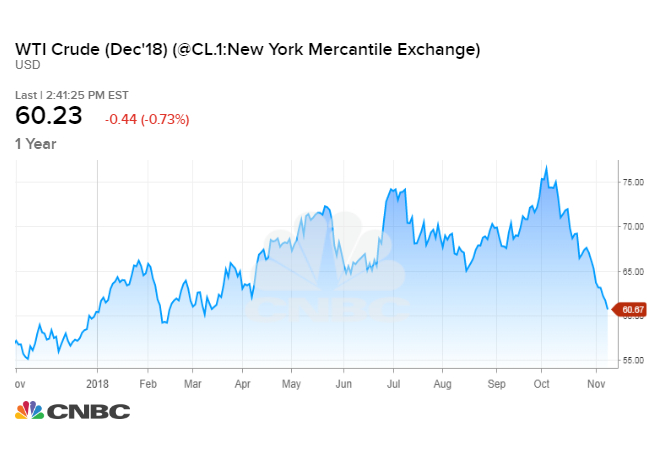

U.S. crude prices fell Friday for a 10th consecutive session, sinking deeper into bear market territory and wiping out the benchmark’s gains for the year.

The 10-day decline is the longest losing streak for U.S. crude since mid-1984, according to Refinitiv data.

Crude futures fell for a fifth straight week as growing output from key producers and a deteriorating outlook for oil demand deepen a sell-off spurred by October’s broader market plunge. The drop marks a stunning reversal from last month, when oil prices hit nearly four-year highs as the market braced for potential shortages once U.S. sanctions on Iran snapped back into place.

“The market’s not tight. I think there are windows where you could perceive it to be tight, and I think the markets got caught into that,” Christian Malek, head of EMEA oil and gas research at J.P. Morgan, told CNBC on Friday. “The reality is that we’re still in a world where we’re overproducing and we’ve got surplus.”

U.S. West Texas Intermediate crude settled 48 cents lower at $60.19 on Friday. The contract is now down nearly half a percent this year. It fell as low $59.26 on Friday, its weakest level in about nine months.

WTI fell into a bear market in the previous session, tumbling more than 20 percent from a nearly four-year high last month at $76.90.

International benchmark Brent crude was trading 39 cents lower at $70.26 by 2:29 p.m. ET, down 19 percent from its recent high. The contract touched a seven-month low at $69.13 on Friday.

Brent has fallen in nine of the last 10 sessions, but is still up more than 4.5 percent this year.

Oil prices spiked in early October on fears that U.S. sanctions on Iran, OPEC’s third biggest oil producer, would thin out global petroleum supplies. However, the Trump administration granted temporary sanctions exemptions to eight countries, allowing Iranian crude exports to continue and easing concern about undersupply.

Analysts now expect the loss of exports from Iran to be less severe than anticipated.

Meanwhile, the world’s top three producers, the United States, Russia and Saudi Arabia are pumping at or near records. Other OPEC members and exporting nations are also turning on the taps.

Preliminary data this week suggests U.S. production has hit an all-time high at 11.6 million barrels per day.

On Friday, oilfield services firm Baker Hughes reported that U.S. drillers added 12 rigs to U.S. oil fields across the country this week, the biggest increase since the end of May, according to oilfield service firm Baker Hughes.

The oil rig count, an indicator of future supply, has broken out of a tight range over the last four weeks. Prior to that, the count bounced around a tight range between 858 and 869 oil rigs for about four months. It now stands at 886 rigs, the highest since March 2015.

However, some analysts think there’s a ceiling on U.S. production growth.

Michael Kelly, head of exploration and production research at Seaport Global Securities, says quarterly earnings report showed that drillers are focused on generating free cash flow and high corporate earnings, rather than growing output at all cost.

“I’m not as fearful now that U.S. growth is going to wreck the party like I was a year ago,” he told CNBC’s “Power Lunch” on Friday. “A year ago I would say 2 million barrels per day growth out of the U.S. is possible. I don’t think that’s the playbook anymore.”

Still, signs that OPEC and several other oil producers including Russia could soon cut output have not put a floor under the market.

About two dozen exporting nations began capping their output in 2017 in order to drain a global crude glut. The group agreed in June to restore some of that output, and producers with spare capacity have been pumping more oil since then.

However, Saudi Arabia and Russia are reportedly in talks to orchestrate another round of cuts.

A committee representing the alliance meets this weekend and could make a production recommendation to the wider group. Last month the Joint Ministerial Monitoring Committee said the group may need to change course and begin cutting production once again.

“This monitoring committee is important, but it looks like consensus is likely to build around what Russia and Saudi decide, and that gets institutionalized,” J.P. Morgan’s Malek said.

[“source=cnbc”]